How Trees Affect Your Homeowners Insurance in Utah

What Tree Damage Is Covered

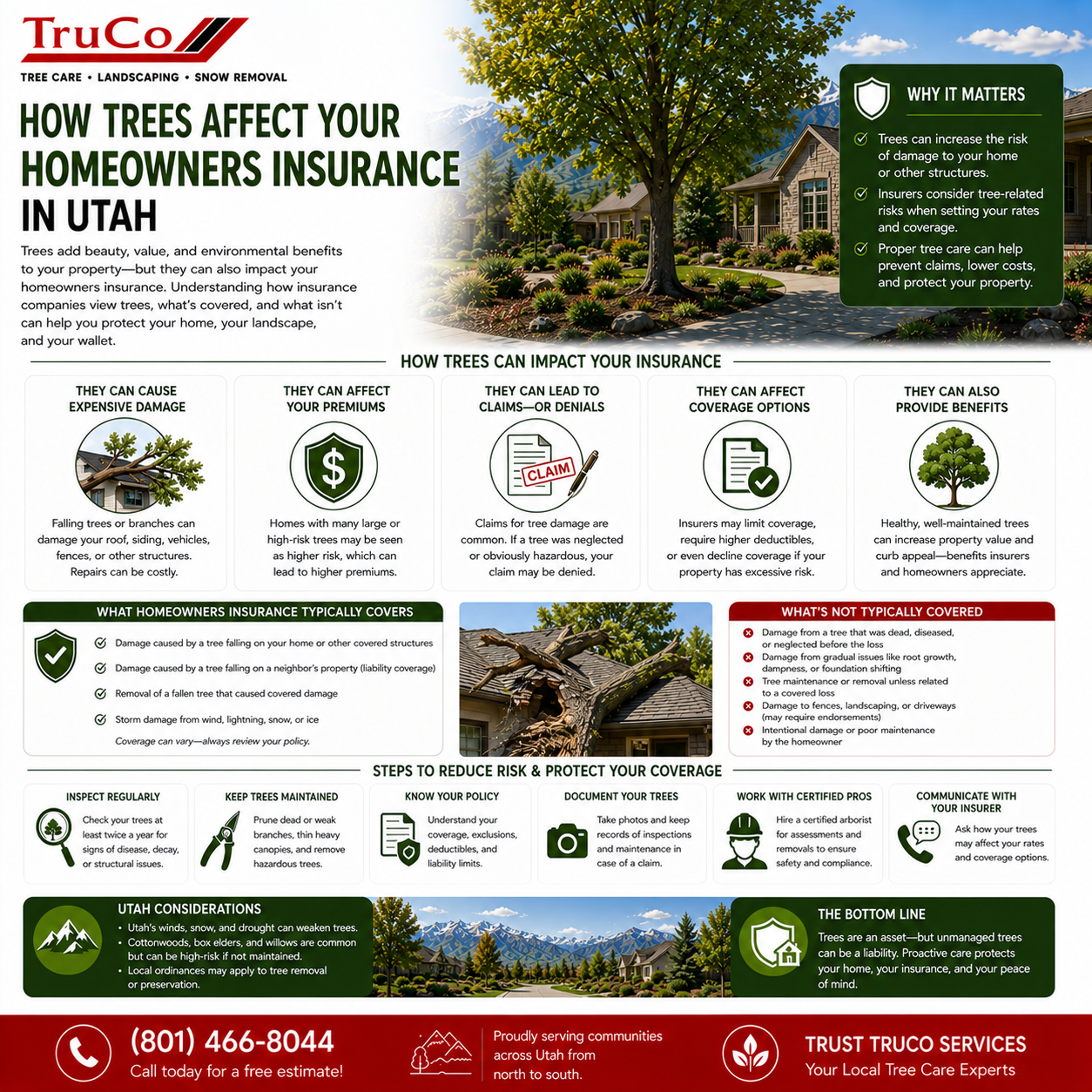

Standard Utah policies cover tree damage from windstorms, hail, lightning, fire, ice/snow weight, and vehicle impact. Typically includes dwelling repairs, detached structures, and personal property. Most policies include $500-$1,000 per tree for removal from a structure after a covered loss.

Other Structures Coverage

Standard HO-3 policies cover other structures at ~10% of dwelling limit. So a $500,000 home has $50,000 for fences, sheds, detached garages. Deductible applies. Some policies have sub-limits for fences. Consider increasing if you have large trees near fence lines.

Liability for Neighbor Damage

Healthy tree + windstorm = neighbor's insurance covers their damage (no-fault). But if your tree was dead/diseased/visibly hazardous, your neighbor can file a liability claim against your policy. Standard liability limits are $100,000-$300,000 — a single large tree on a neighbor's home could exceed this. An umbrella policy is worth considering.

Utah's Shared Liability

Utah follows modified comparative negligence. If both you and neighbor knew about a diseased boundary tree and neither acted, a court might find each 50% at fault. Documentation of inspections and neighbor communications strengthens your position.

What Is NOT Covered

Preventive removal of healthy trees (even if risky). Tree removal if it falls but hits no structure. Landscape replacement (crushed plants). Earth movement damage (landslides, soil erosion along Wasatch Fault are excluded). These are all your responsibility.

Preventative Maintenance

Pruning, dead wood removal, disease treatments — all out-of-pocket. While significant ($500-$1,500 for major pruning), far less than dealing with preventable tree failure. Insurers may deny claims if they determine damage was foreseeable due to lack of maintenance.

How Insurers Assess Risk

Factors: large trees near home (cottonwoods, silver maples, willows), known disease/decay, trees on steep slopes, wildfire zone location. Insurers may require removal as condition of coverage, exclude tree damage, or decline to write policy. This is becoming more common.

Wildfire Risk Impact

WUI areas like Alpine, Draper, Farmington, Park City face higher premiums and stricter requirements. Insurers may require defensible space — thinned trees, removed dead vegetation. Some have stopped writing new policies in high-risk areas. Creating defensible space is far cheaper than losing coverage or your home.

Tips for Filing Claims

Prioritize safety. Don't make major repairs before adjuster inspects. Take extensive photos/video. Obtain tree service estimate for removal. Keep all receipts. Report promptly. Be ready to answer about tree's condition before the incident — inspection records showing the tree was healthy support your claim.

Three Pillars of Protection

1) Regular tree maintenance. 2) Proper documentation. 3) Communication with insurance agent. Review your policy declarations for tree removal sub-limits. Consider umbrella liability if you have large trees.

Frequently Asked Questions

Insurance pay for tree that fell but hit nothing? Generally no. Only covered when tree damages a covered structure.

My tree on neighbor's house? Healthy tree + nature = their insurance. Hazardous tree you ignored = they can claim against your liability.

How much for removal? Typically $500-$1,000 per tree sub-limit. Structural repairs covered separately.

Can insurer require removal? Yes. They can require removal of hazardous trees or cancel/non-renew your policy.

Are trees themselves covered? Not typically. Considered landscaping. Limited to $500/tree for specific perils like fire or lightning.

Should I increase liability? Wise if you have large trees. $100,000-$300,000 might not be enough. Umbrella policies are affordable.